When you’re thinking about the cost of attending college, two terms will pop up repeatedly: “sticker price” and “net price.” Understanding these terms can save you a lot of confusion—and potentially a lot of money.

So, what is the difference between “sticker price” and “net price” for college? Let’s break it down in a way that makes sense and gets straight to the point.

- Sticker Price vs Net Price: Why the Difference Matters

- Sticker Prices and Net Prices at Ivy League Schools

- How Financial Aid Impacts Your Net Price

- Hidden Costs beyond the Sticker Price

- Common Myths about Sticker Price and Net Price

- Practical Tips for Lowering Your Net Price

- Frequently Asked Questions

- Takeaways

Sticker Price vs Net Price: Why the Difference Matters

The difference between sticker price and net price matters because it affects your college decisions. If you focus only on the sticker price, you might dismiss schools that seem too expensive. But when you dig deeper, you’ll realize that many institutions—especially Ivy League schools—offer generous financial aid packages.

For instance, Princeton University’s sticker price is about $84,040, but the average net price for families earning less than $100,000 per year is $12,176. This massive gap shows why you should always look at the net price instead of the sticker price alone.

What is the sticker price for higher education?

The sticker price is the advertised cost of attending a college or university for one academic year. It includes tuition, fees, room, and board, and sometimes other expenses like books or supplies. Think of it as the “full retail price” of college.

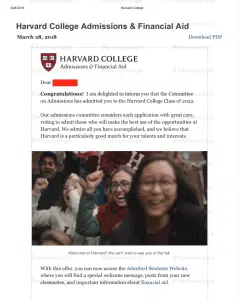

For example, Harvard College’s 2024-2025 sticker price is approximately $82,950. This figure includes $61,676 for tuition and around $21,190 for food and housing. While that number is enough to make anyone’s jaw drop, it’s rarely what students end up paying.

What is the net price?

Net price, on the other hand, is what you actually pay after financial aid, scholarships, and grants are applied. It’s the real cost of college—your out-of-pocket expense. To calculate the net price, take the sticker price and subtract all forms of gift aid.

For example, let’s say you’re accepted to Stanford University. The sticker price for 2024 is $87,833. However, for the average student receiving need-based aid, scholarships and grants bring the net price down to $19,333. That’s a much more manageable number, isn’t it?

Sticker Prices and Net Prices at Ivy League Schools

Here’s a look at the sticker price and average net price at Ivy League schools for the 2024-2025 academic year:

| Ivy League School | Sticker Price (2024-2025) | Average Net Price for Families Earning <$100,000 |

| Harvard University | $82,950 | $14,634 |

| Yale University | $88,430 | $19,266 |

| Princeton University | $62,400 | $12,176 |

| Columbia University | $93,417 | $12,411 |

| University of Pennsylvania | $89,028 | $28,042 |

| Dartmouth College | $87,923 | $21,144 |

| Brown University | $89,489 | $25,520 |

| Cornell University | $88,140 | $29,161 |

This table shows how financial aid significantly reduces the net price for middle-income families.

Why net price calculators are your best friend

Most colleges provide a net price calculator on their websites, a valuable tool that estimates the cost of attendance based on your family’s financial situation. These calculators analyze data like income, household size, and the number of dependents in college to estimate your actual costs after financial aid.

While these calculators are not perfectly precise, they offer a reliable ballpark figure to help you understand what you might pay and avoid making decisions based solely on sticker prices.

For instance, Dartmouth’s net price calculator might indicate that a family earning $60,000 per year could pay just around $5,903 annually for their student’s education. Similarly, Brown University’s calculator might show that a family earning under $100,000 could attend at a significantly reduced cost of $25,520.

This level of transparency allows prospective students and their families to make informed decisions without being deterred by the intimidating sticker price. Using these calculators early in your college search allows you to narrow down schools that align with your financial capabilities and plan accordingly for additional expenses.

How Financial Aid Impacts Your Net Price

When applying to Ivy League schools, it’s important to understand their exceptional financial aid policies. Most are need-blind, meaning your ability to pay doesn’t affect admissions decisions, and they pledge to meet 100% of demonstrated financial need for all admitted students. These policies make elite education accessible to students from all financial backgrounds, ensuring cost isn’t a barrier for talented applicants.

Your net price depends on the type and amount of financial aid you qualify for, which typically falls into two categories:

1. Need-based aid

This aid is determined by your family’s income, assets, and other financial circumstances. Top-tier schools like Harvard, Yale, and MIT are known for their commitment to covering 100% of demonstrated financial need.

Many schools also have no-loan policies, replacing loans with grants to ensure students graduate with minimal debt. Need-based aid ensures that students from low- and middle-income families can access top-tier education without shouldering excessive financial burdens.

2. Merit-based aid

This form of aid is awarded based on academic achievements, athletics, or other areas of excellence. While less common at Ivy League schools, merit-based aid is widely available at many public and private institutions.

Schools like the University of Southern California and Vanderbilt University provide significant merit scholarships to attract top-performing students. Merit-based aid can further reduce the net price and is an important consideration for students with notable talents or exceptional academic records.

Completing applications like the FAFSA (Free Application for Federal Student Aid) and the CSS Profile is essential for accessing financial aid and determining your estimated net price. These forms evaluate your financial situation in detail and are used by colleges to allocate need-based and, in some cases, merit-based aid.

Missing deadlines or providing incomplete information can result in less aid, so preparing and submitting these forms accurately is crucial.

Concrete examples of sticker price vs net price

To better understand the concept of net price, let’s look at two scenarios:

- High-income family. A family earning $200,000 annually with one child attending Columbia University might receive little or no need-based aid. Consequently, they could be responsible for paying close to the full sticker price of $93,417 annually.

However, some families in this income bracket might still receive aid if they have multiple dependents in college or are in unusual financial circumstances.

- Middle-income family. A family earning $85,000 annually with two children in college might qualify for substantial need-based aid. Their net price at Columbia could drop to $20,000—or even lower, depending on other factors like assets and the number of dependents in college.

Due to the generous aid policies of Ivy League schools, families in this income range could see costs reduced to as little as $10,000 annually in some cases.

These examples illustrate the importance of understanding the distinction between the sticker price and the net price when evaluating the affordability of a college education. A school’s advertised tuition might seem out of reach, but your actual cost could be significantly lower after factoring in financial aid.

Hidden Costs beyond the Sticker Price

Even after determining your net price, there are additional expenses to consider that may not be immediately apparent:

- Travel expenses. Travel costs can quickly add up, particularly for students attending out-of-state or Ivy League schools far from home. For instance, a student flying cross-country multiple times a year could incur thousands of dollars in transportation expenses.

- Health insurance. Many colleges require proof of health insurance coverage. If you don’t have adequate coverage, you may need to purchase the college’s plan, which can cost between $2,000 and $4,000 annually.

- Books and supplies. While some financial aid packages include allowances for books and supplies, these costs can still total $1,200 or more per year. Additional expenses for specialized equipment, lab fees, or software may further increase your out-of-pocket costs.

- Personal expenses. Items like laundry, dorm furnishings, and extracurricular activities can add up over the course of the academic year. Budgeting for these smaller but necessary costs is essential to avoid unexpected financial strain.

Understanding and planning for these hidden costs ensures you are fully prepared for the financial commitment of attending college. Researching and leveraging resources like net price calculators, financial aid offices, and scholarships can help bridge the gap between the cost of attendance and your ability to pay.

Common Myths about Sticker Price and Net Price

When it comes to college costs, misconceptions about sticker price and net price can prevent families from exploring affordable options. Let’s debunk some common myths to help you make informed decisions.

Myth 1: Only rich families can afford Ivy League schools.

Reality: Many Ivy League schools are more affordable for middle-income families than public universities. Generous financial aid policies often mean families earning less than $100,000 pay minimal amounts. These schools use endowments to subsidize tuition costs, leveling the playing field for students from diverse socioeconomic backgrounds.

Myth 2: The sticker price is non-negotiable.

Reality: While you can’t haggle like you’re buying a car, financial aid can drastically reduce costs. Some families even successfully appeal their aid packages to secure more funds. This is especially true if you have competing offers from similarly ranked institutions.

Myth 3: Net price calculators aren’t worth the time.

Reality: They’re one of the most useful tools for estimating your actual costs. They can help you eliminate financial surprises before applying. Taking 15 minutes to use this tool can save you thousands of dollars—or even lead you to a school you thought was unaffordable.

Practical Tips for Lowering Your Net Price

Affording college can feel daunting, but most students don’t pay the full sticker price thanks to scholarships, grants, and financial aid. By applying strategic tips, you can maximize aid, reduce costs, and negotiate better offers to make higher education more affordable without overwhelming debt.

Here are five ways to lower your net price and reduce the financial burden of attending college:

1. Apply for scholarships.

Look for external scholarships to reduce your out-of-pocket expenses. Start with local organizations, as there’s often less competition. Also, keep track of application deadlines and requirements to ensure you maximize your chances.

2. Choose schools with generous aid.

Research colleges that are known for their generous financial aid. Ivy League schools and elite liberal arts colleges often lead in this area. For example, Amherst College has been ranked among the top schools for need-based financial aid, with most students paying far less than the sticker price.

3. Submit your FAFSA early.

The FAFSA (Free Application for Federal Student Aid) and some types of aid like the Pell Grant are distributed on a first-come, first-served basis. Don’t delay! Missing the priority deadline by a week can reduce your chances of getting state or institutional aid.

4 . Negotiate your aid package.

Let your top choice know if another school offers you a better deal. Schools sometimes adjust aid to match competing offers. Be polite but firm in your request, and be ready to share documentation of the competing offer.

5. Limit non-essential costs.

Stick to a budget for dining out, entertainment, and travel expenses. Cutting back on these smaller costs can save you hundreds, which adds up over time.

Breaking down financial aid policies by region

Financial aid varies significantly depending on the type of school and its location. For example:

- East coast private universities. Schools like Harvard and Yale often offer some of the most robust need-based financial aid packages. These institutions have large endowments, allowing them to provide aid that meets 100% of demonstrated financial need. Families earning less than $100,000 annually often pay little to no tuition at these schools.

- West coast universities. Institutions like Stanford and the University of California system have different approaches. Stanford provides substantial aid similar to the Ivy League schools, while UC schools focus on in-state affordability, offering lower tuition rates for California residents and grants like the Cal Grant.

- Midwest liberal arts colleges. Schools like Grinnell and Carleton often provide generous merit-based aid and need-based assistance. This makes them attractive options for students with strong academic or extracurricular records.

Frequently Asked Questions

1. How do I find the net price for my dream college?

Use the net price calculator available on the college’s website. It will estimate your costs based on your financial situation, giving you a clearer picture of what you’ll actually pay.

2. Can the net price change after my first year?

Yes, the net price can fluctuate if your financial circumstances change. For example, if your family’s income decreases, you may qualify for more aid. However, maintaining eligibility could be a condition if you receive merit-based scholarships tied to performance.

3. Are public colleges always cheaper than Ivy League schools?

Not necessarily. While public colleges often have lower sticker prices, Ivy League schools might be cheaper due to their generous financial aid packages. Always compare net prices, not sticker prices.

4. Can international students access financial aid?

Yes, but it varies by institution. Many Ivy League schools offer need-based aid to international students, but policies differ, so check with each school directly. Public universities may have fewer options.

5. What’s the difference between loans and grants in financial aid?

Grants are free money you don’t have to repay, while loans must be repaid with interest. Prioritize grants and scholarships over loans to minimize debt.

Takeaways

- Always compare net prices when evaluating schools. The sticker price rarely reflects what you’ll pay.

- Take advantage of these tools to estimate your real costs upfront.

- Research what each school offers to determine your best options.

- Apply early for aid, consider scholarships, and budget wisely to reduce your overall costs.

- Need some help with calculating the net price for your dream college? Consult an admissions counselor for help.

Author